A personal-vehicle accident shows up on your CDL-linked MVR and triggers a commercial-driver surcharge tier even when you weren't driving a truck. Here's how the cross-record reporting works and what it costs.

Your Personal Auto Policy Already Knows You Hold a CDL

When you apply for personal auto insurance, carriers ask whether you hold a commercial driver's license. If you answer yes, your policy is underwritten in a commercial-driver risk tier from day one, typically 8-15% higher than a non-CDL holder with an identical driving record.

The premium difference exists because CDL holders drive more total miles annually and face occupational exposure that correlates with higher at-fault accident rates in statistical loss models. This surcharge applies whether you drive a truck 60 hours a week or you hold a CDL for seasonal work and drive a personal sedan the rest of the year.

If you answer no during application and the carrier later discovers the CDL through an MVR pull at renewal, the policy can be rescinded retroactively or non-renewed for material misrepresentation. Disclosure is not optional under current state insurance fraud statutes.

How a Personal-Vehicle Accident Appears on Your CDL-Linked MVR

Your state DMV maintains a single motor vehicle record tied to your driver's license number. If you hold a CDL, that same record supports both your commercial license endorsements and your personal driving history. There is no separate personal-use-only record.

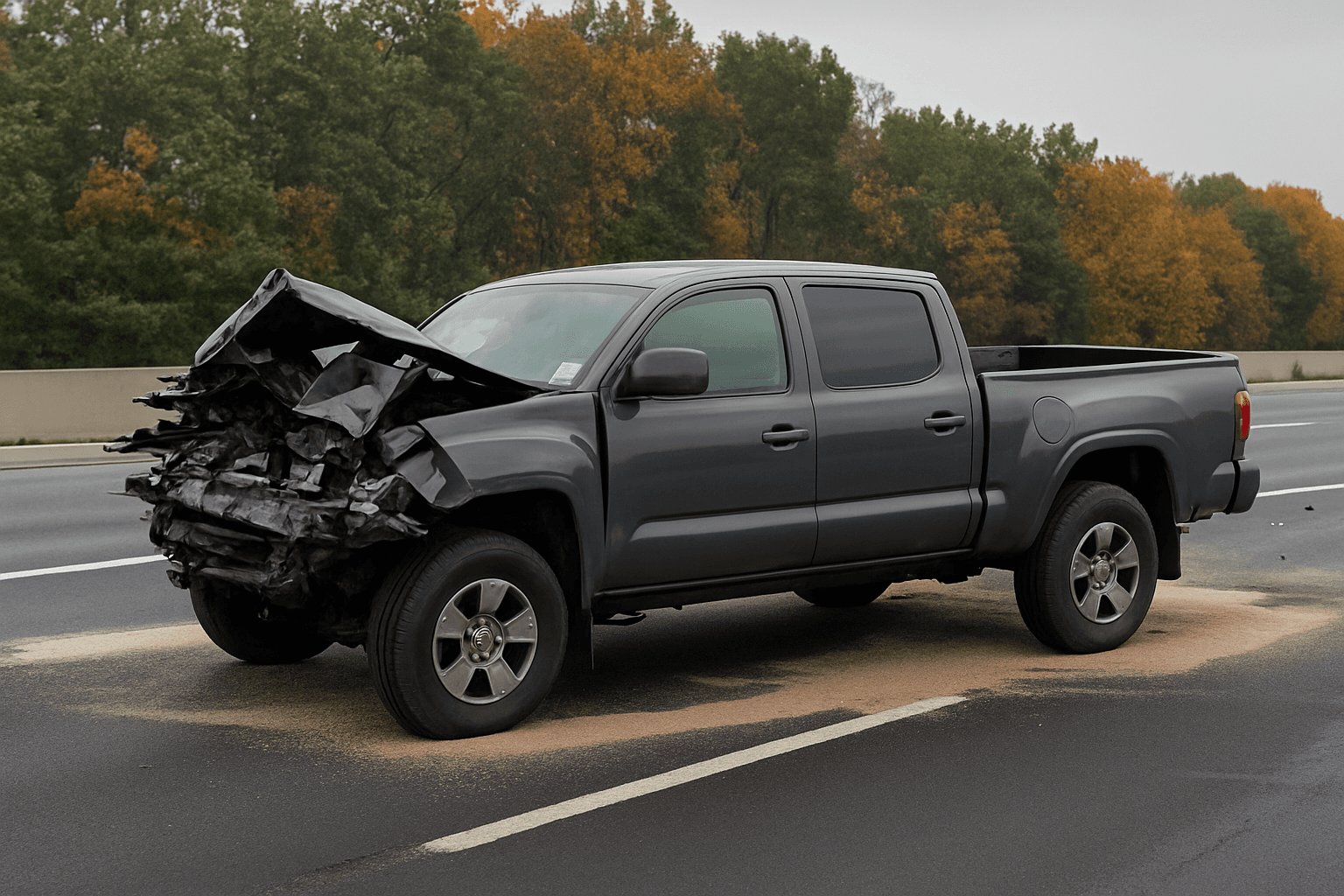

When you have an at-fault accident in your personal vehicle, the responding officer files a crash report with the DMV. The DMV posts the accident to your MVR within 30-60 days. Because your CDL is linked to that MVR, the accident becomes visible to both your personal auto carrier and your employer or any future trucking company that pulls your FMCSA Pre-Employment Screening Program record.

Most states do not distinguish between personal and commercial vehicle use when posting accidents to the MVR. The record shows the date, fault determination, and vehicle type, but the accident contributes to your total violation count regardless of which vehicle you were driving.

Compare rates from carriers that work with drivers who have points

Standard carriers surcharge heavily after violations. These specialists price your specific record differently.

Get Your Free Quote✓ Violation Specialists✓ No Obligation✓ Licensed Carriers✓ All Point Levels

What the Commercial-Driver Surcharge Multiplier Costs You

Personal auto carriers apply a base at-fault accident surcharge of 20-40% for non-CDL drivers, depending on state and severity. For CDL holders, that same accident triggers a commercial-driver surcharge multiplier that adds an additional 10-25% on top of the base accident surcharge.

A driver with a clean record paying $120/mo who has a personal-vehicle at-fault accident might see rates increase to $168/mo with a 40% base surcharge. A CDL holder in the same scenario pays $193/mo because the commercial-driver multiplier compounds the base surcharge. The total increase is 61% instead of 40%.

This surcharge structure lasts for three to five years depending on the carrier's lookback period. The commercial-driver multiplier does not drop off early even if you surrender your CDL, because the accident occurred while you held the license and the carrier's actuarial tables classify the loss event as a commercial-driver claim.

Why Employer FMCSA Monitoring Picks Up Personal Accidents

Trucking companies are required under FMCSA regulations to monitor driver MVRs annually and review any new violations or accidents. When your personal-vehicle accident posts to your state MVR, it becomes visible in your FMCSA Pre-Employment Screening Program record within 10 business days.

Your employer does not distinguish between personal and commercial accidents when evaluating continued insurability under their commercial auto policy. Most fleet policies include driver-qualification standards that disqualify any driver with two at-fault accidents in a 36-month period, regardless of vehicle type.

If the personal accident is your second moving violation or at-fault loss in three years, you may be removed from the roster and reassigned to non-driving duties or terminated depending on the company's safety policy. The accident does not have to involve a commercial vehicle to trigger this consequence.

Whether You Can Appeal the Surcharge or Separate the Records

You cannot petition your state DMV to remove a validly reported at-fault accident from your MVR, and you cannot request a CDL-excluded personal driving record. The MVR is a unified document under state vehicle codes, and separation would require legislative change to the record-keeping statute.

Some carriers allow you to appeal the commercial-driver multiplier if you provide proof that you no longer hold an active CDL and have not driven commercially in the past 12 months. The appeal does not remove the base accident surcharge, only the incremental commercial-driver risk loading. Approval rates for these appeals are low, and most carriers require CDL surrender documentation from the state DMV.

Your only leverage point is shopping carriers at renewal. Not all personal auto carriers apply the same commercial-driver multiplier, and some non-standard carriers do not differentiate between CDL and non-CDL surcharge schedules because their entire book is already priced for elevated risk.

What Happens If You Don't Disclose the Accident to Your Employer

FMCSA regulations require you to report any traffic violation or accident to your employer within 30 days, regardless of whether it occurred in a personal or commercial vehicle. Failure to report is a recordkeeping violation that can result in disqualification under 49 CFR 383.31.

Your employer will discover the accident when they pull your annual MVR or when their commercial auto carrier runs a renewal underwriting report. At that point, the failure to disclose becomes a terminable offense under most trucking company safety policies, separate from the accident itself.

If the accident results in a citation or conviction, you are also required to notify your employer within 30 days of the conviction date. The notification window is shorter than the DMV posting timeline, so waiting for the MVR to update does not satisfy the disclosure rule.

How Long the Accident Affects Your Personal Auto Rate

Personal auto carriers apply accident surcharges for three to five years depending on state regulation and company underwriting guidelines. The surcharge begins at your first renewal after the accident posts to your MVR, not the accident date.

In most states, the accident remains on your MVR for three years from the date of the incident. Carriers in states with three-year lookback windows will remove the surcharge at the renewal following the three-year anniversary. Carriers in states with five-year lookback windows continue the surcharge for two additional years even after the DMV record clears.

The commercial-driver multiplier follows the same timeline as the base accident surcharge. If you surrender your CDL during the surcharge period, some carriers will remove the multiplier at the next renewal, but the base accident surcharge remains in effect until the full lookback period expires.