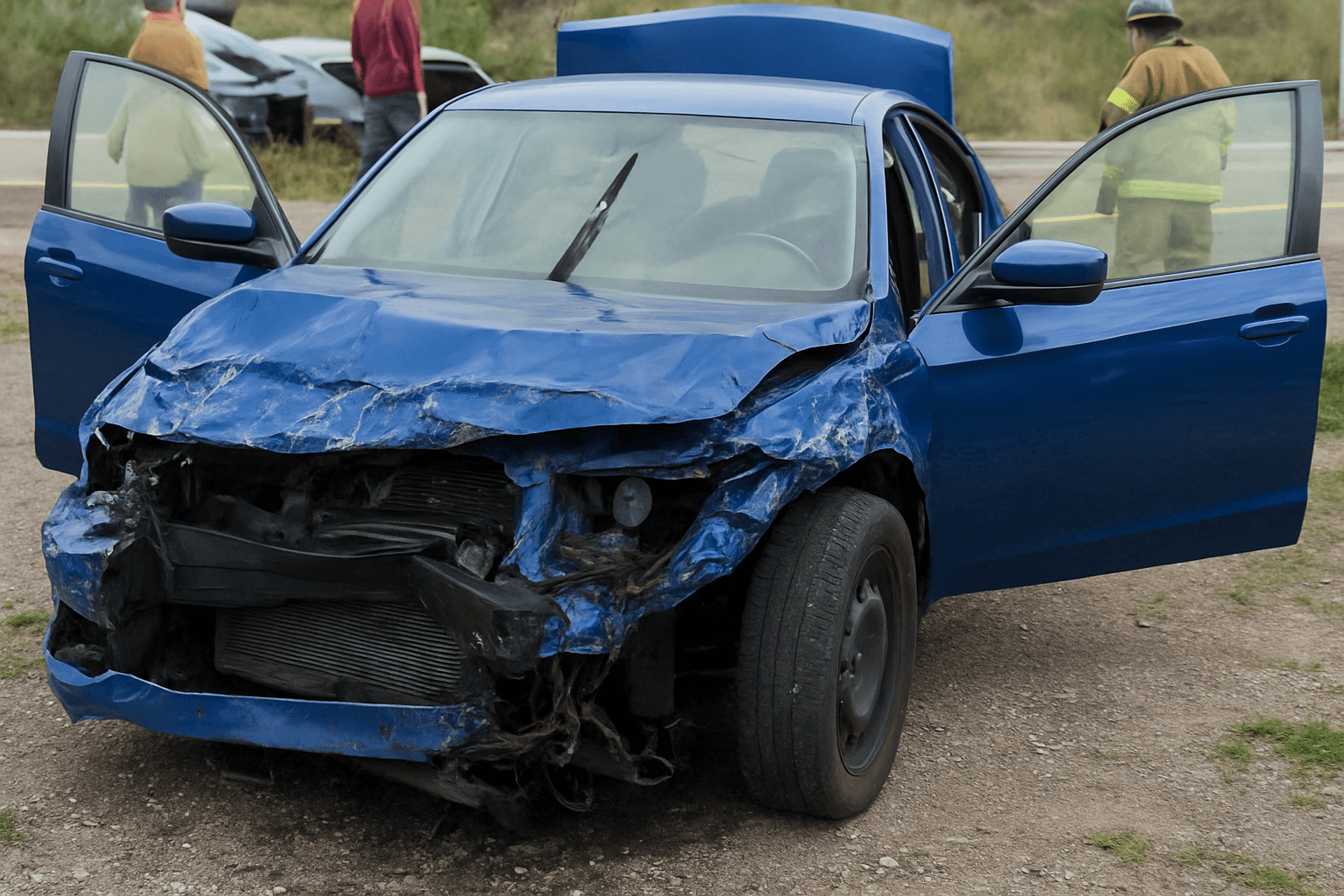

North Carolina adds 4 points to your license for an at-fault accident and insurance carriers use a separate 3-year surcharge schedule that typically raises rates 30-50%. Switching carriers before renewal can reduce that impact.

Why Switching Immediately After an At-Fault Accident Often Saves Money

Your current carrier applies accident surcharges at renewal, not the day the accident happens. Most NC carriers use a flat 30-50% surcharge for a first at-fault accident that lasts 3 years from the accident date, but the base rate they apply that surcharge to varies widely between carriers.

If you switch before your renewal date, you avoid your current carrier's post-accident renewal quote entirely. The new carrier prices the accident into your quote from day one, but their base rate and surcharge structure may produce a lower total premium than your current carrier's surcharged renewal. Progressive and Geico typically apply smaller accident surcharges than State Farm or Allstate for first-time at-fault accidents in North Carolina.

Timing matters because NC law requires carriers to use your driving record as of the quote date. If you request quotes 2 weeks after the accident, the accident appears on your motor vehicle record and every carrier prices it. Waiting until renewal means your current carrier has already calculated the surcharge and you lose the opportunity to compare their post-accident pricing against competitors before committing to another 6-month term.

What Happens to Your NC Driving Record After an At-Fault Accident

North Carolina adds 4 points to your license for an at-fault accident resulting in more than $3,400 in property damage or any bodily injury. The points stay on your DMV record for 3 years from the accident date. You reach the 12-point suspension threshold if you accumulate 8 additional points within 3 years, which means a second at-fault accident or two speeding tickets of 15+ mph over the limit would trigger a suspension.

Insurance surcharges operate on a separate timeline. Carriers review your record at each renewal and apply surcharges based on violations and accidents within their lookback period, typically 3 years in North Carolina. Your accident surcharge begins at your first renewal after the accident and continues for 3 years from the accident date, not the renewal date.

The DMV conviction date and the carrier surcharge start date rarely align. If your accident occurred 4 months before renewal, you pay the surcharge for 2 years and 8 months after renewal. If you switch carriers 1 month after the accident, the new carrier applies the surcharge immediately but you avoid 3 months of coverage at your old carrier's higher rate.

Compare rates from carriers that work with drivers who have points

Standard carriers surcharge heavily after violations. These specialists price your specific record differently.

Get Your Free Quote✓ Violation Specialists✓ No Obligation✓ Licensed Carriers✓ All Point Levels

Which NC Carriers Write Policies for Drivers with One At-Fault Accident

State Farm, Allstate, and Nationwide remain in the preferred market for a single at-fault accident with no other violations, but they apply the steepest surcharges in North Carolina — typically 40-50% for 3 years. Progressive and Geico classify single-accident drivers as standard risk and apply 25-35% surcharges, often producing lower total premiums despite identical coverage.

Liberty Mutual and Travelers accept single-accident drivers but route them to standard-tier pricing, which raises base rates before the accident surcharge applies. The combined effect usually exceeds Progressive's accident-specific pricing unless you carried unusually high liability limits that benefit from Travelers' multi-policy discount structure.

Nationwide and Erie operate direct and agent channels in North Carolina with different underwriting rules. The direct channel declines drivers with 6 or more points, but a single 4-point accident qualifies. The agent channel allows up to 8 points but applies a standard-market surcharge that can exceed direct pricing by 15-20%. Request quotes from both channels because the pricing gap for accident-only records often favors direct.

How to Request Quotes Without Triggering Multiple Credit Pulls

North Carolina carriers use credit-based insurance scores as a rating factor, and each quote request can generate a soft inquiry that does not affect your credit score or a hard inquiry that does. Most direct carriers, including Progressive, Geico, and Nationwide's direct channel, use soft inquiries for online quotes. State Farm and Allstate agents typically pull credit as a hard inquiry when binding a policy, not when quoting.

Request all quotes within a 14-day window. Credit bureaus treat multiple auto insurance inquiries within 14 days as a single event for FICO score purposes, even if some carriers use hard pulls. This window starts from the first inquiry date, not the accident date.

You can decline credit-based pricing in North Carolina, but carriers then assign you a neutral score that typically raises your premium 10-20% compared to your actual score if your credit is above 650. Drivers with credit scores below 600 sometimes save by declining credit-based pricing, but the math varies by carrier. Progressive and Geico allow you to request quotes both ways and compare.

What Coverage Limits Make Sense After a 4-Point Accident

North Carolina's minimum liability limits are $30,000 per person, $60,000 per accident for bodily injury, and $25,000 for property damage. These minimums do not change after an accident, but staying at minimums after an at-fault accident increases your financial exposure if you cause a second accident before points fall off.

Carriers price liability increases differently for pointed drivers. A step from $30,000/$60,000 to $100,000/$300,000 bodily injury coverage adds 15-25% to your base premium, but the accident surcharge applies to the higher base. If your post-accident quote is $140/mo at minimums, moving to $100,000/$300,000 raises it to $160-$175/mo, not a simple percentage of the original premium.

Uninsured motorist coverage in North Carolina must match your liability limits unless you reject it in writing. If you raise bodily injury liability to $100,000/$300,000, uninsured motorist coverage increases automatically and the combined premium impact is 20-30% above minimum coverage. That increase compounds with the accident surcharge, but it also protects you if an uninsured driver causes a second accident while your record is already pointed.

When the At-Fault Accident Triggers SR-22 Filing Requirements

A standard at-fault accident does not require SR-22 filing in North Carolina. SR-22 filing applies when your license is suspended for points and you need to reinstate, or when the court orders it as a condition of probation after a DUI or reckless driving conviction.

If your at-fault accident combined with existing points pushes you to 12 points, your license suspends and reinstatement requires SR-22 for 3 years. The filing itself costs $50 with most carriers, but SR-22 status reclassifies you as high-risk and moves you from standard to non-standard pricing. Expect premiums 60-100% higher than standard accident-only pricing.

Progressive, Geico, and Acceptance Insurance write SR-22 policies in North Carolina for pointed drivers. State Farm and Allstate write SR-22 for existing customers but decline new applicants who need filing. If you need SR-22, request quotes from Progressive and Acceptance first because their non-standard divisions specialize in reinstatement cases and price more competitively than agents trying to place you in a standard carrier's high-risk tier.

How Long Accident Surcharges Last and When Rates Recover

North Carolina carriers apply accident surcharges for 3 years from the accident date, but the surcharge percentage often decreases each year. Progressive and Geico typically reduce the surcharge by one-third at each annual anniversary: 30% in year one, 20% in year two, 10% in year three. State Farm and Allstate hold the full surcharge for the entire 3-year period.

Your rate does not automatically drop when the accident falls off your record. Carriers review your driving history at renewal, so the surcharge removal happens at your first renewal after the 3-year mark. If your accident occurred on March 15, 2022, and your policy renews every April 1, the surcharge drops at your April 1, 2025 renewal.

Shopping again at the 3-year mark accelerates rate recovery. Once the accident ages off, you requalify for preferred pricing with carriers that declined you or priced you in standard tiers immediately after the accident. Drivers who switched to Progressive post-accident often save another 15-25% by moving back to State Farm or Nationwide once the record clears, because those carriers' clean-record pricing undercuts Progressive's standard rates.