Your premium just jumped 20-40% after a single at-fault claim. Here's the exact month-by-month timeline for when surcharges drop and how to accelerate rate recovery.

What happens to your rate in the first 30 days after an at-fault accident

Most carriers do not apply an accident surcharge until your policy renews, which means you have a 0-to-12-month window between the accident date and the rate increase depending on where you are in your current policy term. If your accident occurs 2 months before renewal, the surcharge appears in 60 days. If it occurs 2 weeks after renewal, you have 11.5 months at your current rate.

Carriers with accident-forgiveness programs waive the first at-fault accident surcharge entirely, but eligibility typically requires 3-5 years of continuous coverage with that carrier and a clean record during that period. If you switched carriers within the past 3 years or already have a speeding ticket on record, accident forgiveness does not apply and the surcharge will hit at renewal.

The accident enters your CLUE report within 30 days of the claim filing date. Every carrier you shop will see it for the next 5-7 years regardless of whether you stay with your current insurer or switch. The lookback period for accident surcharges is 3-5 years depending on the carrier, but the CLUE record persists longer and can still affect underwriting decisions even after the surcharge period ends.

Months 1-12: The surcharge appears and peaks

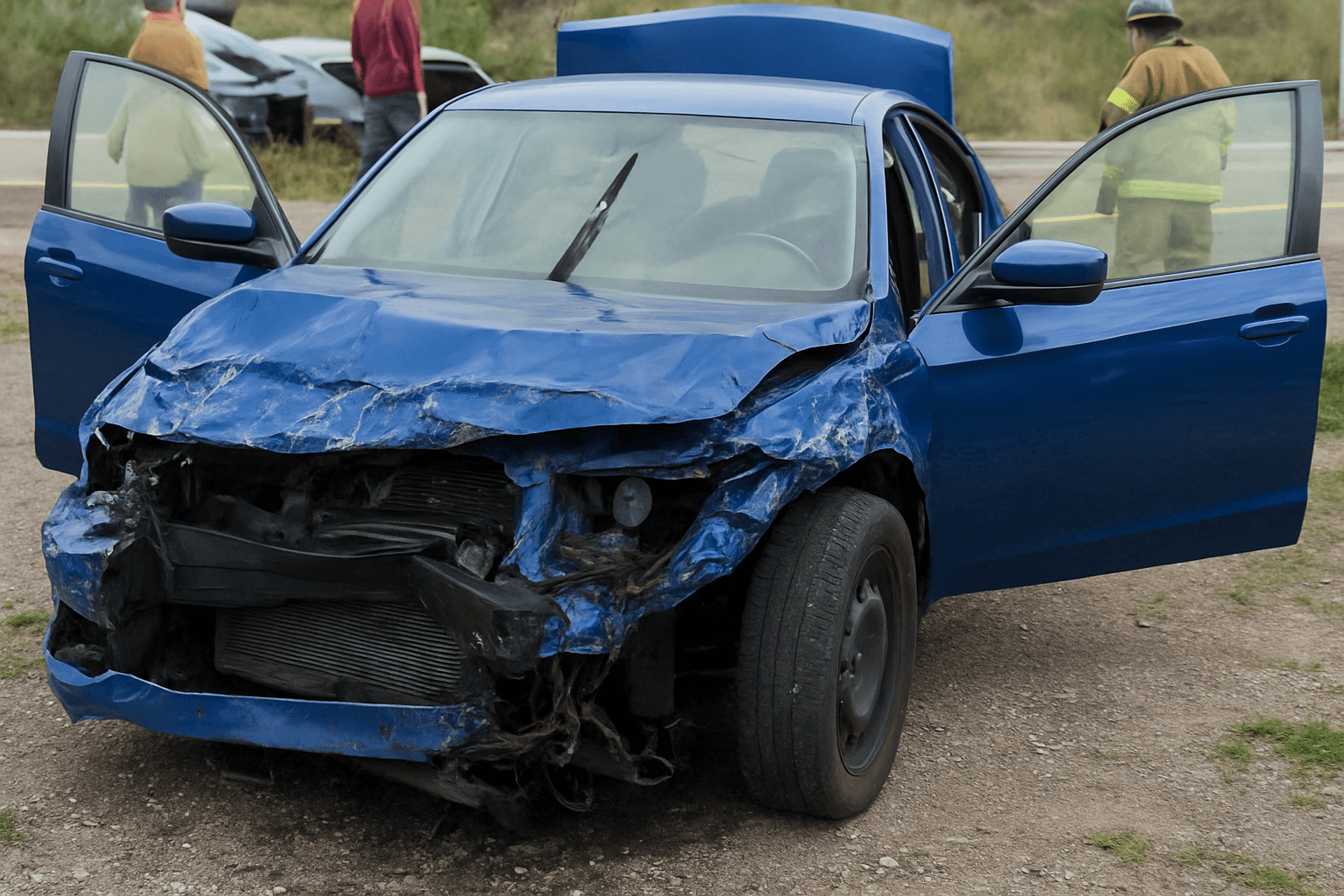

At your first renewal after the accident, your premium increases by 20-50% depending on the carrier, the claim amount, and your prior record. A single at-fault accident with $5,000 in property damage typically triggers a 20-30% increase. An accident with bodily injury or a claim over $10,000 can push the surcharge to 40-50%. Carriers with tiered rating systems may also move you from a preferred tier to a standard tier, which compounds the surcharge with a base rate increase.

The surcharge applies to your full premium, not just liability coverage. If you carried collision and comprehensive coverage at the time of the accident, both coverages reflect the surcharged rate. Dropping collision to reduce costs eliminates the coverage you are now statistically more likely to need, and most lenders require collision coverage on financed vehicles regardless of your driving record.

This is the most expensive 12-month period of the recovery timeline. The surcharge is fully loaded, you have not yet crossed any carrier-specific tier-down thresholds, and your accident is still recent enough that competing carriers treat it as a primary rating factor. Shopping at month 6 or month 10 rarely produces a better rate than your current carrier because every insurer is applying a similar surcharge to a similar base rate.

Compare rates from carriers that work with drivers who have points

Standard carriers surcharge heavily after violations. These specialists price your specific record differently.

Get Your Free Quote✓ Violation Specialists✓ No Obligation✓ Licensed Carriers✓ All Point Levels

Months 13-36: Surcharge persists but shopping windows open

Most carriers hold the accident surcharge at full strength for 36 months from the accident date, not the renewal date. If your accident occurred on March 15, 2022, the surcharge begins to drop at your first renewal on or after March 15, 2025, even if that renewal falls in May or June. Carriers calculate the surcharge period from the accident date, which means your third renewal after the accident may still carry partial surcharge depending on the timing.

Some carriers tier down the surcharge incrementally at 24 or 30 months for drivers with no additional violations during the surcharge period. A 40% surcharge at month 12 may drop to 25% at month 24 and 10% at month 30 before disappearing entirely at month 36. Other carriers apply the full surcharge for the entire 36-month window and remove it completely at the end. Your declaration page does not itemize surcharge schedules, so most drivers do not know which model their carrier uses until they see the renewal quote.

Shopping at month 24 or month 30 can surface carriers that tier based on time-since-accident rather than applying a binary surcharge. If your current carrier holds the full increase until month 36 and a competing carrier tiers down at month 24, switching at your 24-month renewal can cut 12 months off your high-rate period. The rate difference rarely appears unless you request quotes from at least 3 carriers, because the first carrier you call may use the same surcharge model as your current insurer.

Months 37-60: Lookback window narrows and rates normalize

At 36 months after the accident date, most carriers remove the surcharge entirely and your base rate returns to the tier you qualified for before the accident, assuming no additional violations occurred during the surcharge period. If you added a speeding ticket at month 18 or a second at-fault accident at month 28, the new violation resets the surcharge clock and you remain in a surcharged tier for another 36 months from the new violation date.

Your rate at month 37 will not match your rate at month 0 because base rates increase annually for all drivers regardless of claims history. A driver who paid $1,200 per year before an accident in 2022 and sees the surcharge drop in 2025 should expect a post-surcharge rate of $1,350-$1,450 per year, reflecting 3 years of inflationary base rate increases across the market.

Some carriers continue to factor the accident into tier placement until the full 60-month lookback window closes, even after removing the explicit surcharge. A driver may see the 40% surcharge disappear at month 36 but remain in a standard tier rather than returning to a preferred tier until month 60. The tier difference typically adds 10-15% to the base rate, which is significantly lower than the surcharge but still measurable. Shopping at month 36, month 48, and month 60 ensures you are not leaving tier-based savings on the table as the accident ages out of different carriers' underwriting models.

Actions that accelerate rate recovery during the surcharge period

Completing a defensive driving course removes 2-3 points from your DMV record in most states, but it does not automatically remove an accident surcharge from your insurance rate. Carriers treat DMV point removal and claims-based surcharges as separate rating factors. The course may qualify you for a 5-10% defensive driver discount, which offsets part of the surcharge, but you must request the discount explicitly at renewal and provide the completion certificate. Most carriers do not apply the discount retroactively.

Increasing your liability limits or adding umbrella coverage signals lower risk to underwriting systems and can move you into a preferred tier faster than maintaining state minimums. A driver who increases bodily injury liability from 25/50 to 100/300 at the first post-accident renewal may qualify for a tier upgrade at month 24 rather than month 36, depending on the carrier's underwriting guidelines. The higher limits add $10-$20 per month to the premium, but the tier upgrade can reduce the base rate by 10-15%, producing a net savings of $30-$50 per month for the remainder of the surcharge period.

Bundling auto and home or renters insurance with the same carrier unlocks multi-policy discounts that range from 10-25% depending on the insurer. For a pointed-record driver carrying a 40% accident surcharge, a 15% bundle discount reduces the effective surcharge to 25%, cutting the monthly cost by $40-$60. The bundle discount persists after the surcharge drops, compounding the savings into the post-surcharge period. Most carriers require both policies to renew simultaneously to maintain the discount, so coordinating renewal dates at the time of the accident can maximize the discount window.

When to shop and when to stay during the recovery timeline

Shopping in months 1-12 after an accident rarely improves your rate because every carrier applies a similar surcharge to recent at-fault claims. The accident appears on your CLUE report immediately, and competing insurers price the risk identically to your current carrier. The only exception is when your current carrier non-renews your policy due to multiple claims in a short period, which forces you into the non-standard market regardless of timing.

The highest-value shopping windows occur at month 24, month 36, and month 60 after the accident date. At month 24, you can identify carriers that tier down surcharges incrementally rather than holding them flat for 36 months. At month 36, you can confirm that your current carrier has fully removed the surcharge and compare your post-surcharge rate to competitors who may tier based on time-since-accident rather than binary lookback windows. At month 60, you can capture preferred-tier pricing from carriers that factor accidents into underwriting beyond the surcharge period.

Staying with your current carrier for the full surcharge period makes sense only if they offer accident forgiveness, incremental tier-downs, or loyalty discounts that offset the surcharge faster than switching. Most carriers do not disclose surcharge schedules in policy documents, so the only way to know whether you are on an incremental or flat surcharge model is to request a quote from a competing carrier at month 24 and compare the effective monthly cost. If the competitor is $40 per month cheaper, your current carrier is using a flat model and switching saves $480 per year for the remainder of the surcharge period.